A New Economic: Situational Examples, Sample Numbers, and Loan/Pension Diagrams

Here are three situational examples of how “A New Economic” works, with sample numbers to gain a ballpark idea of what the outcome would be for the parties involved in each case. They are arranged from the more simple to the more complex.

The first covers the properties utilized by a single working adult, the loan status of each property, and the respective “creditors” (the individuals or institutions that share ownership of said properties).

The second looks at the properties utilized by a family of four, the loan status of each property, and the creditors.

The third explores the properties of a company, in this case, an airline, their loan statuses, and the creditors. Included is the subject of pensions, and how they fit into the plan.

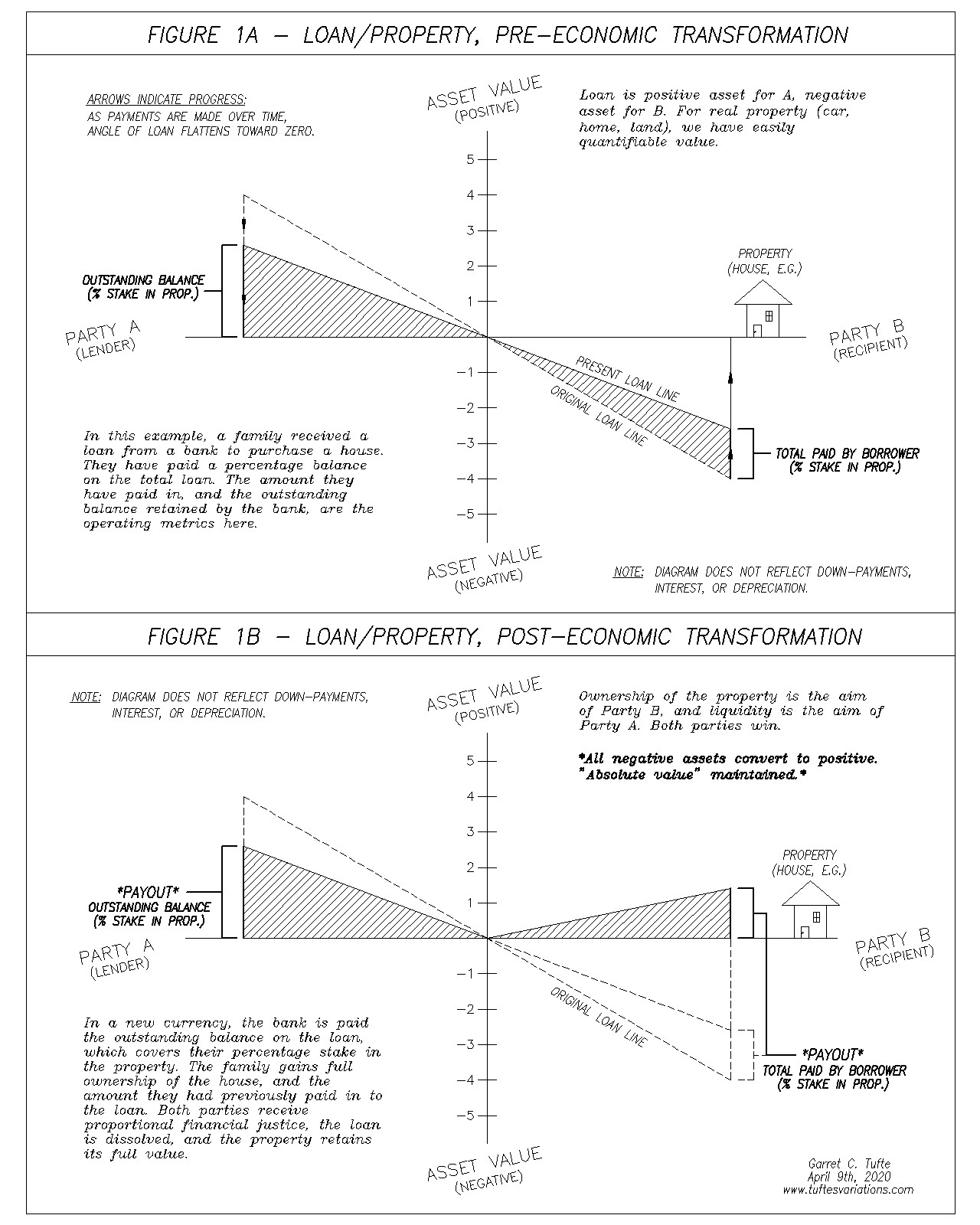

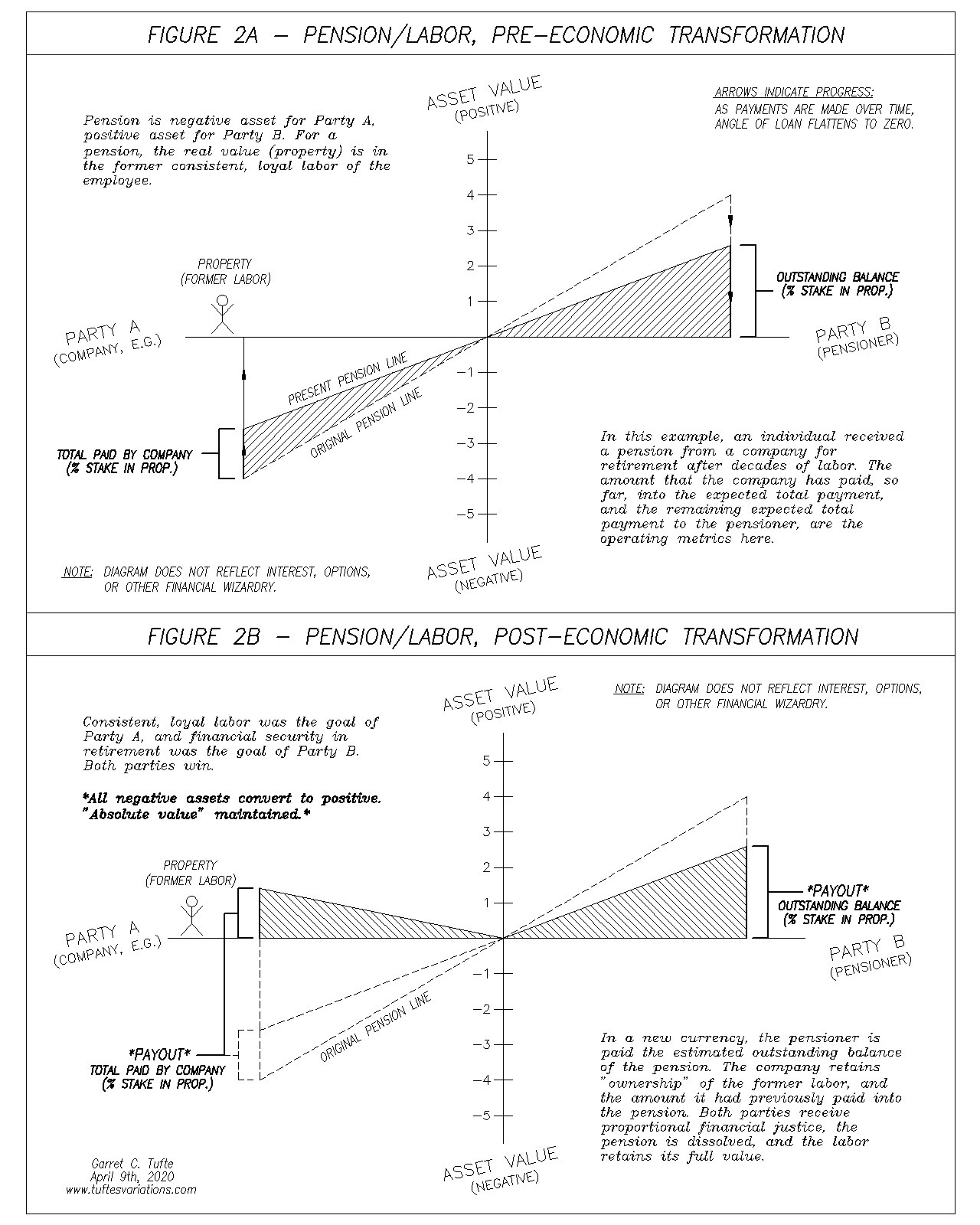

Below these samples are four diagrams which help to show the relationship between “Loan/Property” (diagrams with “1”) and “Pension/Labor” (diagrams with “2”) at present (diagrams with “A”), and post-economic transformation (diagrams with “B”).

This is a helpful primer to further understand the mechanisms of this plan, to see the “systemizability” of it, and how YOU can figure just how much you stand to gain. So, get settled, grab a calculator, a pencil and some paper, and let’s get down to business!

EXAMPLE NO. 1

Sample properties utilized by a young adult:

1 car – 2 years paid on a 5-year loan – Creditor: a local credit union – Appraised value: $17,000

1 bedroom studio apartment – a rental – Creditor: a private landlord – Appraised value: $120,000

The car has shared ownership between the credit union and the individual. He has so far paid in $6,800 (a 40% stake), while the credit union retains an outstanding balance of $10,200 (a 60% stake). The fellow receives ownership of the car and 6,800 in the new currency. The credit union receives 10,200 in the new currency.

The renter lives at the property in question, and the landlord lives elsewhere. The apartment’s appraised value is $120,000. The renter receives ownership of the apartment, and his landlord receives 120,000 in the new currency.

So, the individual receives:

1 car (from himself and the credit union)

1 apartment (from his former landlord)

and 6,800 in the new currency

The credit union receives:

10,200 in the new currency

The landlord receives:

120,000 in the new currency

That was example number 1. Super simple stuff here. The renter receives the properties that he utilizes, others with a stake in them receive financial justice, all negative assets are converted to positive, each property retains its full value, and the agreements between the parties (the loan and rental agreement, in this case) are dissolved. Everybody wins! And then we all get on with our lives.

EXAMPLE NO. 2

Sample properties utilized by a family of four:

1 car – fully owned by the couple. Creditor: Themselves (calling them their own creditor is for a “consistency of logic”, and the purpose behind this will become more apparent as we go forward.)

~ the car is registered and appraised at $12,000. The couple receives 12,000 in the new currency.

1 truck – 2 years into a 4-year lease. Creditor: A self-financed local dealership

~ the truck is registered and appraised at $15,000. The couple has paid $150 monthly installments for 2 years, for a total of $3,600. The dealership thus retains $15,000 worth of stake in the property, as the truck would have been returned to them at the conclusion of the agreement. The couple receives the truck. The dealership receives 15,000 in the new currency. (These are the basic numbers.)

1 3-bedroom home – 5 years paid into a 15-year mortgage. Creditor: A regional bank

~ the home is appraised at $250,000. The couple has paid $1,400 per month for 60 months, for a total of $84,000. The couple receives the home and 84,000 in the new currency. The bank receives 166,000 in the new currency. (Again, these are basic numbers. If you want to get really technical, throw in a down payment, interest payments, appraised value upon signage, depreciation, and see what you get using the principle logic.)

In sum, the family receives:

their car (from themselves)

their truck (from themselves and the dealership)

their house (from themselves and the bank)

and a total of 96,000 in the new currency

The dealership receives:

15,000 in the new currency

The bank receives:

166,000 in the new currency

The family keeps the properties they utilize and whatever they paid into them (if on a “rent-to-own” basis. Each agreement has its own details to be adhered to), and the creditors receive the remainder value of each property in cash. Fresh cash. Like, really, REALLY fresh cash.

Okay! That was example number 2.

EXAMPLE NO. 3

Sample properties utilized by an airline:

After a few basic informational searches, appraisal figures on properties or assets *necessarily* “owned, rented, or leased” by an airline are difficult to find online, especially considering my limited internet access at present. So please understand that the numbers themselves are speculative figures, used only for the purpose of showing proportional relationship between them, rather than concrete, stand-alone figures.

That being said, for anyone who IS privy to such details, they may certainly calculate a rough resultant financial position of the company and its creditors by examining a sample of factors:

Properties utilized by an sample airline:

2 small aircraft – owned by the company – Creditor: itself

3 large passenger aircraft – 7 years into a 10 year ownership agreement – Creditor: a large central bank

Pension liability – owned by the company – Creditor: 12 former employees

(Note: Pension liability is a negative asset for the company, and a positive asset for the former employees. This is the first I have mentioned pensions, and they work in an inverse manner to loans, as it relates to individuals. The diagrams below are a useful tool to understand this relationship. It is helpful to look at pensions as installment payments for the “property” of labor, of which the company had formerly used. The distribution of the full value of the contract, similarly, is then based on the amount paid by the company thus far (to err on the side of positivity, the company would then get that amount in cash in the new currency), and the “remaining balance”, a mean estimation of remaining future payment to each individual (each individual would receive this amount in the new currency).)

Okay, still with me? Let’s run some numbers:

2 small aircraft – Each are worth $3,000,000, giving a total of $6,000,000. The company retains ownership of the aircraft and receives 6,000,000 in the new currency.

3 large passenger jets – Each are worth $50M, and the company has paid off 7 of 10 years worth. The company receives 70% of $150M total = 105M in the new currency. The bank retains 30% stake in the aircraft, and so receives 45M in the new currency. The company receives full ownership of the jets.

Pension liability for 12 former employees – Depending on age and former salary, the estimated remaining balance for each pension will vary significantly. For simplicity’s sake, we will take a median dollar amount and a median estimated length of continued payment. Of 12 pensioners, 6 receive $2000/month and 6 receive $1200/month, giving a median of $1600/month, or $19,200/year. The estimated amount of time of continued payment (until the person passes away), has 6 pensions with 8 years likely, and 6 pensions with 16 years likely, giving an average of 12 years. 12 years x $19,200/year = $230,400/pension on average. With 12 of them, we have an original, total liability of $2,764,800. If the company has paid 1/3 of the total amount so far, the compensation for the company, in the new currency comes to: 0.33 x 2,764,800 = 912,384 in the new currency. Each pensioner would receive the remaining balance on the estimated years of continued payout based on their individual contracts, averaged, here, to be .67 x $230,400 = 154,368 per pensioner, on average, in the new currency.

In sum,

The airline receives:

2 small aircraft (from itself)

3 large passenger jets (from itself and the big bank)

6M + 105M + 912,384 = for a total of 111,912,384 in the new currency

The bank receives:

45,000,000 in the new currency

Each pensioner receives:

On average, 154,368 in the new currency.

All past contracts, loans, and pension agreements between these parties may then be dissolved, and they may all get on with their lives in a fresh economy.

Okay, that’s it for the examples. You made it through!

LOAN/PROPERTY and PENSION/LABOR DIAGRAMS:

ADDENDUM:

I think, by now, you get the picture, on the “systemizability” of these propositions, and just how easy it is to figure the just ownership and payout of most situations. In addition, I should like to say, that this plan is exactly what is needed to fix the tremendous economic damage that is presently wrecking the United States and much of the world with the present virus panic. This plan would allow anyone and everyone to *voluntarily* sequester themselves, in the event of a dangerous pathogen wreaking havoc, rather than receiving the brunt of authoritarian measures. This is a consequence of the “radical freedom” I spoke of in the video: security in residential ownership, freedom from needing to subject oneself to harmful work environments, etc.

Okay, that’s it for now.

Much love and spread the good word!

Whether from myself or anyone else.

A new world beckons!

Heed the call.

– G